Do you believe in Insurance?

I never really believe in Insurance (or perhaps was brought up by my mum not to believe in them). My mum always said "保险都是骗人的" since i was young and those views was ingrained even though her views was a tad too extreme. Probably she was "bugged" by over-zealous insurance agents trying to sell her useless policies but maybe she was right.... because instead of buying policies, you should be buying the insurance company. 😁 That was how Warren Buffet became extremely rich by using "free money" from insurance premiums to invest.

Warren Buffett was able to build his fortune in two primary ways: by owning private companies that generate large amounts of income for him to deploy, and by entering the insurance business to get his hands on cheap investment capital. Warren Buffett abhorred debt; it wasn't his style to borrow money at 5% and try to invest it at 12% (Munger, meanwhile, built his large fortune by taking out margin loans to amplify his high conviction stock picks). Instead, Warren Buffett used the "free money" provided by insurance premiums allowed Buffett to use leverage—by investing the money for a return before he had to pay the money back to those making successful insurance claims, Buffett was able to use this spread to build quick wealth.... source

When did I buy my first insurance policy?

As i mentioned earlier, i was brought up not to believe in insurance. How did i ended up with my first policy then? 🤔

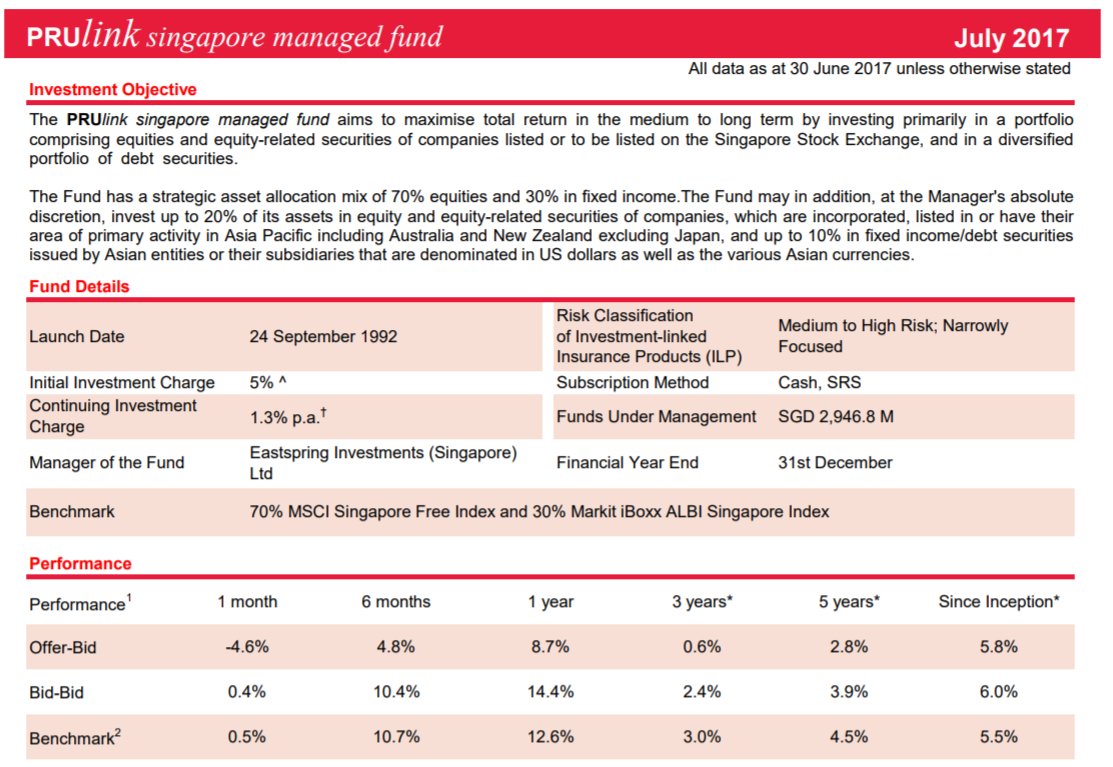

I bought my first policy when i was in the army. The agent was from Prudential and he was an ex-army sign-on who became an insurance after he left service. He basically convinced the whole group of us into buying the investment-linked policy ("ILP") which offers direct exposure to the Singapore stock market because history has shown that stock market will outperform the rest. The fund is Prulink Singapore Managed Fund and the fact sheet is here. Actually he was not wrong. My premium would have compounded at around 5.8% annually since inception and the return would have been decent.

For simplicity, assuming i put in $1,200 at the start of every year and it compounds at 5.8%, my premium paid of $28,800 would turn into $59,624 today after 24 years! Unfortunately, my surrender value today is only $30,680 (death benefit is now ~$75,000)... so what exactly went "wrong"?

Reason 1 - My agent asked me to increase my sum assured protection from $5,000 to $45,000 but this protection may not have come at a very high cost vis-a-vis a term insurance

My agent called me one year into the purchase and said that i should increase the sum assured to $45,000 so that if anything happens to me, my family would receive some payout. Well, he wasn't wrong, except that it was a huge price to pay as the premium eats into the amount set aside for investment returns. Well, you can't have the best of both worlds can you?🤔

Reason 2 - When i started working, i decided to switch the fund from Singapore Managed Fund to Global Managed Fund and the latter under-performed big time. I think this is one of the biggest mistake i made in the ILP. I should just left the exposure to the Singapore market and my surrender value today would have been much higher.

The fund size for the Global Managed Fund is small and the returns of 2.4% paled in comparison to the Singapore Managed Fund.

So how did my ILP performed after all these years. Let's take a look.... the premium paid of $28,800 turned into a surrender value $30,680.... Working backwards on the surrender value, it means that my premium was being compounded at 1% annually and that is worse than buying a life policy.

Assuming a life policy protects and compounds at the 10 year government Singapore Savings Bonds of 2.12%, the surrender value should have been at least $37,046... meaning that the ILP returns has severely under-performed due to the two reasons mentioned above. ILP is probably a black hole.... a huge part of the premium goes towards paying for some critical rider every year and only a small balance was used to purchase units in the fund.

When did i buy my second policy?

I bought my second policy from NTUC Income when my first kid was born for the both of us. Let's see how that performed. My sum assured was around $50,000 and the premium paid was $21,473 but the surrender value is $25,272. The NTUC Income Life Policy somewhat has performed slightly more respectably at 1.8% compounded interest than Prudential.

Am i going to get a third policy?

The answer is yes but this time round it is different and I hope i am much wiser now. 😂

As my life progressed to 40s, the original policies taken when i am in the early stage of my life are no longer adequate. I have a family to think about and a mortgage to take care of should something happens to me. At the same time, i have been gradually building up my retirement portfolio so as i assess my current situation, what is important is that the family is taken care of should something bad happens to me. Do i intend to get a life policy again for coverage? The answer is no as it is just too expensive a product. My intention is to buy term and invest the rest of the money instead of relying on the insurance company to do that for me.

The third policy that I will be getting will be a term insurance that pays a lump sum of $500,000 for permanent disability🤕 , 36 critical illness 🤒 and death 😇 from now till i turn 70.

It is interesting to note that the premium is still relatively low if you pay till 60 years old and it escalates up exponentially beyond 60 years old. This is all about probability as insurance policies are 'underwritten' by actuary. While the good news is that i can terminate the term policy at any time, the downside is that the premiums has zero "returns" should you live beyond 70 and Singaporeans has one of the longest life expectancy in the world at 82 years old! 😂

The reason why i stopped the coverage at 70 is that it gets prohibitively expensive beyond that and i believe i will be happy to "go' once i live past 70 years old and hopefully at that point in life, I will have adequate passive income for life.

So here is the poll question for today....once i have the 3rd policy in place, i will have adequate coverage. What do you think i should do with my ILP with Prudential? Take the poll here.

Let me know what you think and i will update you on my next course of action when it has taken place. 😎

Happy Insuring !

For mortgage, use a separate reducing term insurance --- it's much cheaper & cleaner to not mix with other insurance meant for dependents or ownself.

ReplyDeleteIf you're still operational NSman, you can top up using the Mindef/MHA group insurance which is relatively cheap up to 65 yrs old.

Insurance is a risk management tool & expense. It mustn't be seen as "savings" or "investment". Hence when you no longer have dependents e.g. parents, kids grown up & graduated etc, you don't need large sum assured life insurance anymore. You may not need till 70.

What you continue to need as you age will be those hospitalization plans, long-term care (e.g. Eldershield-type).

Regarding critical illness plans or riders, most people think it's meant to cover treatment costs. WRONG!! The main purpose is to cover your potential lost income, when you're too ill/damaged to continue working. The treatment costs should be covered by appropriate Shield plans + Medisave.

Therefore, if you're not working for income & have no dependents, CI insurance is basically superfluous expense. But some people may want to continue for psychological "security blanket" purpose.

I would keep until it matures, as the return still compounds while provides some protection.

ReplyDeleteAs ILP has flexibility, how about reducing the premium to minimum for current coverage and invest the premium saved and monitor the cash value till it start to drop (at least you get the coverage with lower premium). Or if you do not need the coverage then terminate it (1st Option).

ReplyDelete